Indian Agriculture—if COVID-19 Hadn’t Happened

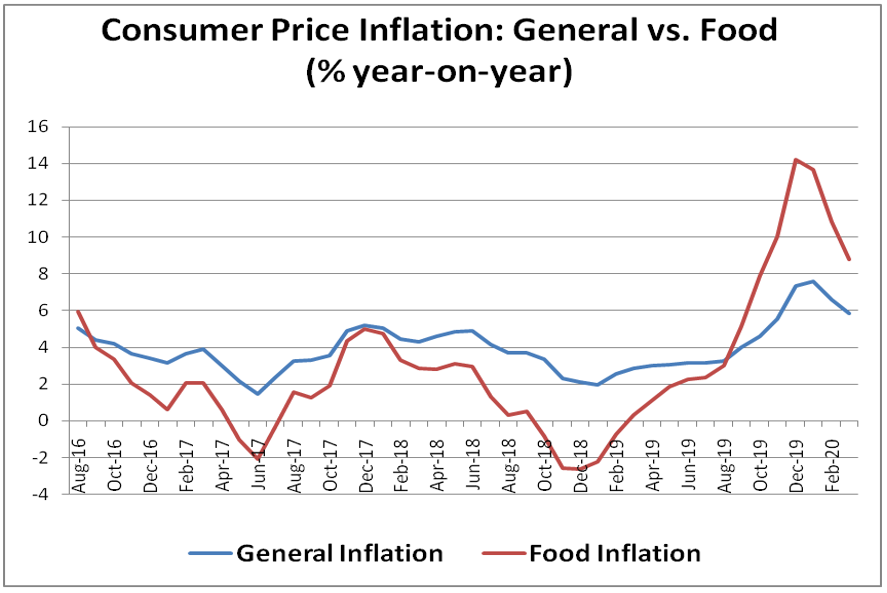

Before COVID-19 struck, the worst seemed over for Indian agriculture. This sector, unlike the rest of the economy, was probably even on the road to recovery, mainly because of prices. Between September 2016 and August 2019, consumer food price inflation consistently ruled below overall retail inflation. That unprecedented 36-months-in-a-row phenomenon ended with the former surging from 2.99 percent year-on-year in August to 5.11 percent, 7.89 percent, 10.01 percent, 14.19 percent and 13.63 percent in the subsequent five months (see chart below). The December retail food inflation figure of 14.19 percent was, in fact, the highest since the 17.89 percent recorded in November 2013.

But it wasn’t just domestic prices.

In January 2020, the United Nations’ Food and Agriculture Organization’s (FAO) global Food Price Index (base year 2002-04=100) reached 183 points, the highest after 185.8 in December 2014. The recovery in international prices reflected supply tightness building up in many commodities. In February, the US Department of Agriculture projected global ending stocks of palm oil for October 2019 to September 2020 to be the lowest after 2009-10. In December, the Dutch financial services giant Rabobank forecast a world sugar supply deficit of 8.2 million tons (mt) in 2019-20, the largest in four years. Skimmed milk powder (SMP) prices at New Zealand’s Global Dairy Trade auctions in December-January, likewise, averaged over $3,000 per ton, a level last seen in August 2014. The average export price of 5 percent broken white rice from Thailand, at $ 493.5 per ton in March was also the highest after July 2013.

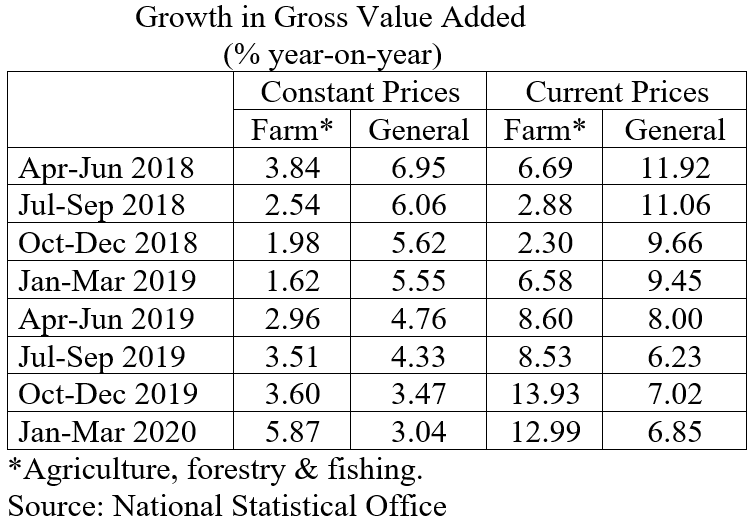

Simply put, the worst deflationary phase for India’s farmers—from previous “multiple coronas,” including the global commodity crash in 2014-15 and 2015-16, the adoption of an “inflation targeting” monetary policy framework by the Reserve Bank of India in February 2015, and finally, demonetization in November 2016—had almost become a thing of the past before COVID-19 entered the scene. This was also partly captured in the quarterly estimates of gross domestic product released by the National Statistical Office. The table below shows farm sector growth surpassing overall growth during the last two quarters of 2019-20 not only in real, but also nominal terms after factoring in inflation.

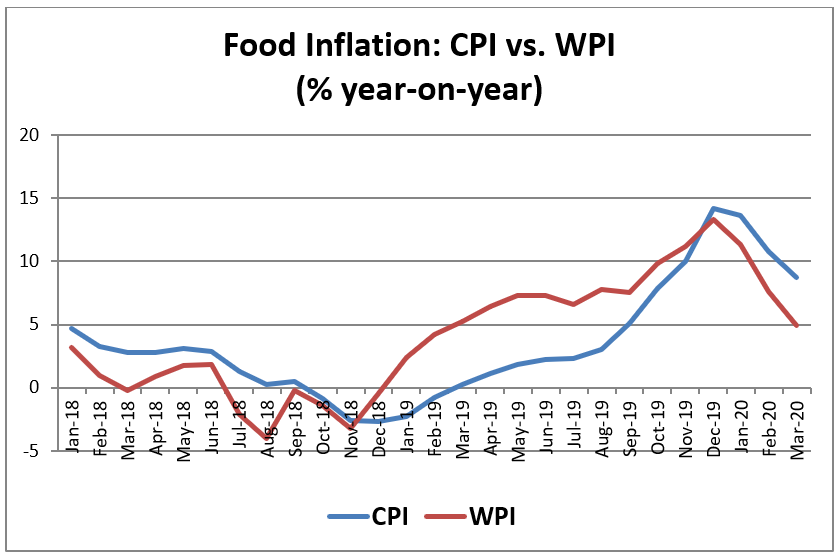

Furthermore, the chart below indicates that inflation in food articles based on the wholesale price index, which matters more to producers, started rising about six months before getting reflected at the retail consumer end.

Prices aside, the outlook was equally favorable regarding production; 2019 was the best rainfall year for India in 25 years. Moreover, much of it was concentrated in the second half, with every month from July to January 2020 registering surplus precipitation. The abundant late monsoon, as well as post-monsoon rains, led to a recharging of groundwater tables and aquifers, along with the major dam reservoirs getting filled to near capacity. The impact of this was mainly on the rabi (winter-spring crop). Farmers expanded rabi acreages by 9.5 percent and a good winter also helped boost yields.

All in all, a turnaround in prices, coupled with bumper rabi production prospects, augured well for farmers. This ideal combination appeared a far cry from the recent past when they had to bear the brunt of both drought (2014, 2015, and 2018) and low produce realizations. Those expectations, unfortunately, haven’t materialized.

Demand Destruction

It all began with poultry around mid-January, when reports of the spread of the novel coronavirus in China were gathering momentum. In this case, a collapse in farmgate prices of broiler birds—from Rs 80-85 per kg to Rs 40-42 towards the second week of February and Rs 30-32 by early March—was triggered purely by unsubstantiated rumors about chicken meat consumption posing the risk of COVID-19. Official clarifications, on poultry products not being found responsible for COVID-19 transmission or its earlier Severe Acute and Middle East Respiratory Syndrome (SARS/MERS) avatars, did little to quell this misinformation campaign over WhatsApp, Facebook, and other social media.

However, the real crisis came only after the all-India lockdown that the Modi government imposed, starting on March 25, the effects of which extended way beyond poultry. The lockdown forced the closure of HORECA (hotels, restaurants, and catering services) businesses, in addition to hostels and canteens. And with wedding receptions and other public functions not taking place, out-of-home food consumption practically came to a halt. The share of such consumption in India has been reckoned at 45 percent for poultry meat—many people who eat chicken aren’t regular “non-vegetarians” at home—and 25 percent in eggs (which are also offered in midday meals in now-shut schools). As consumption and prices plunged, the country’s monthly production of broilers came down from an average of 30 crore (300 million) live birds in January to 11-12 crore (110-120 million) by May, and from roughly 900 crore (9 billion) to 700 crore (7 billion) eggs over the same period. This resulted in lower demand for poultry feed and ingredients, notably maize. According to the Agriculture Ministry’s portal, wholesale prices of maize across India averaged Rs 1,913.21 per 100 kg in January. In May, this had dropped to Rs 1,434.48, while below the Rs 1,921.25 of May 2019. Rabi maize has hardly fetched Rs 1,250 per 100 kg this time in the Gulabbagh market of Bihar’s Purnia district.

This demand destruction story has been replicated across other farm produce, including the ones hitherto experiencing significant output shortfalls. That, in normal circumstances, should have translated into higher prices, but this didn’t happen. A couple examples are worth noting. Take potatoes, where only an estimated 36 crore (360 million) bags (of 50 kg each) from the main rabi crop harvested in February-March were stocked this time in cold stores, as opposed to 48 crore (480 million) in 2019, 46 crore (460 million) in 2018, and the all-time-high 57 crore (570 million) bags of the 2017 post-demonetization crop. Yet, prices of mota aloo or the regular large potato sold from cold stores at Agra in Uttar Pradesh, which were about Rs 21 per kg until early April, had dipped to Rs 17 by the end of May.

The effect on milk has been even more dramatic. 2019-20 was a year when India’s milk production fell for the first time in decades. Until mid-March, there was talk of the country having to import up to one lakh ton (one hundred thousand tons) of SMP, especially to meet demand during the summer months when milk flow from the udders of animals also reduces. Before the lockdown, dairies were selling SMP at Rs 300-320, butter at Rs 290-310, and cheese at Rs 350 per kg. But by the end of May, these had nosedived to Rs 170-180, Rs 230-240, and Rs 225-250 per kg, respectively. Low realizations, in turn, forced dairies to slash prices paid to farmers from Rs 31-32 to Rs 21-22 per liter for cow milk (with 3.5 percent fat and 8.5 percent solids-not-fat content) and from Rs 43-46 to Rs 31-33 per liter in the case of buffalo milk (6.5 percent fat and 9 percent SNF).

The reasons were the same. Potatoes and milk are consumed in home kitchens. That consumption wouldn’t have changed much. The initial few days post lockdown, if anything, witnessed panic-buying, as households sought to stock up extra kilos or liters of vegetables, atta, dal, bread, milk, and edible oil. The lockdown, however, dealt a body blow to all out-of-home and institutional consumption. Thus, consumption of potato-based snacks at roadside joints and eateries—from aloo chaat, tikki, samosa, and pav bhaji to masala dosa and French fries—took a knock. So did the offtake of milk by tea stalls and HORECA businesses, SMP and butter fat by ice-cream manufacturers, khoa and chhena by sweetmeat sellers, and cheese by the likes of Domino’s Pizza, McDonald’s, and Pizza Hut.

What COVID-19 and the lockdown had basically done was “flatten” agricultural produce prices through a leftward shift in the demand curve; this wasn’t about demand reduction on account of prices going up. Rather, with consumption being limited to homes—manpower shortages forced most food companies, as well, to curtail production in factories and, hence, cut raw material purchases—there was less demand now than before even at the same price.

In sugar and edible oils, the hit to institutional consumption—whether from aerated soft drinks, sweetmeat, confectionary and snack makers, or street food vendors and dhabas—proved a major demand dampener. This was further exacerbated by a renewed decline in international prices.

The FAO’s Food Price Index had climbed to a 61-month-high of 183 points in January. By May, it slipped to a 17-month-low of 162.5 points. In sugar and edible oils, though, there was an additional factor at play. On April 20, West Texas Intermediate crude prices closed at an unprecedented minus $37.63 per barrel, from $61.06 at the start of 2020. A day later, raw sugar futures at New York tumbled to 9.75 cents a pound—the lowest since June 9, 2008—after having reached 15.78 cents on February 12. Crude palm oil prices in Malaysia had a similar rollercoaster ride from a calendar-year-high of 3,134 ringgits per ton on January 10 to 1,946 ringgits by May 6.

Two things need to be noted here. The first is the link with crude—the juice from crushing cane can be crystallized into sugar or fermented into ethanol for blending with petrol. When oil prices are high, mills, particularly in Brazil, would want to manufacture more ethanol than sugar. So, when crude prices crashed, the very prospect of Brazilian mills producing an extra 8-9 mt of sugar in 2020-21 was enough to bring down the world market. The same logic applied to palm oil, which has a dual use as a cooking medium and as feedstock for biodiesel. The second point is that both sugar and palm oil were predicted to be in short supply when the year began. These global deficits have vanished post-COVID-19, as have the hopes of Indian sugar mills, which were, until February, well-poised to achieve an export target of 5.5-6 mt for the year ending in September, and rapeseed-mustard farmers, who should have realized better prices for their harvested rabi crop.

COVID-19 has done pretty much what demonetization or notebandi did three years ago. Both hit when farmers had produced bumper crops and wreaked damage by shifting the demand curves leftward. Notebandi caused a hemorrhaging of liquidity from produce markets predominantly transacting in cash. The constraint then was cash, not buyers. In the lockdown, or gharbandi, the crisis has been due to a lack of buyers themselves, restricted now largely to households eating at home. Even their consumption would have been affected because of falling incomes (in respect of poor and lower middle class families) and reduced food requirement from forced inactivity (vis-à-vis, the rich and better off).

The end result was the same: demand destruction. Consumers normally pay more for tomatoes in summer months. But this time around, wholesale prices at Karnataka’s Kolar market averaged Rs 327 per 100 kg in April and Rs 436 in May, compared to Rs 1,440 and Rs 2,068 for the corresponding months of 2019. And dairy farmers received lower procurement prices for milk during the “lean” summer than in the “flush” winter-spring season.

What Next?

Notwithstanding the similarities, there are differences between the situations brought about by gharbandi and notebandi. To start with, agriculture had already gone through tough times when demonetization happened, with back-to-back droughts in 2014 and 2015 on top of the end of a decade-long global commodity boom. Demonetization turned that into a full-blown agrarian crisis, even as its impact on the rest of the economy wasn’t as bad or was, at worst, transitory. With the lockdown, it was quite the opposite. The entire manufacturing sector and services industry—including organized and listed firms that actually benefited from demonetization and Goods and Services Tax at the expense of informal enterprises—had entered slowdown territory from 2018-19, which intensified just when agriculture was showing signs of recovery before the lockdown. The latter hurt the farm sector less, not in the least because agricultural operations—from harvesting and sale of produce in primary wholesale markets, to their intra and inter-state movement—were exempted from gharbandi restrictions.

The second difference has to do with government response, which bordered on the cavalier during notebandi, a time when the Modi government had fully embraced inflation targeting. The Essential Commodities Act (ECA) was given a new lease on life, with onions and potatoes brought under it to enable action against so-called hoarders. Stockholding limits were also imposed on pulses and sugar, alongside trade policy measures allowing duty-free imports even while placing curbs on exports. The period from 2015-16 to 2017-18 saw record imports of pulses and edible oil, despite farmers substantially stepping up domestic production after 2016-17. Import restrictions were introduced only in late-2017, partly in reaction to growing agrarian unrest.

By contrast, the Modi government’s approach during the lockdown has been far more proactive. One reason could be the realization that agriculture—besides being “essential” for supplying food during a public health emergency—offered itself as the only worthwhile economic activity possible under the extant circumstances. The steps taken, including those of local administrations after initial hiccups, to permit movement of labor and machines ensured that farmers could harvest their wheat, mustard, chickpea, or sugarcane. They, no doubt, suffered losses in milk sales and other perishable produce ranging from tomatoes, carrots, capsicum, and gourds to grapes, bananas, watermelons, and totapuri mangoes. But government agencies have also undertaken large-scale procurement of wheat (a record 38.2 mt with a minimum support price value of over Rs 735,000 million), paddy (15.2 mt valued at Rs 275,000 million), pulses (2 mt-plus of chickpea and pigeon-pea valued at Rs 105,000 million), and rapeseed-mustard (0.8 mt worth Rs 35,000 million) in the current rabi marketing season. Together, with another Rs 166,000 million of cash payments under the PM-Kisan direct benefit transfer program, liquidity in excess of Rs 1,300 billion would have been pumped into the farm economy, post-lockdown, through government spending alone.

Overall, it can be said that the Modi government has acquitted itself better in dealing with agriculture-related issues during the lockdown, unlike at the time of demonization when it was caught napping. This apparent change can also be explained by the farm sector being the lone performer in today’s economy. Retail fertilizer sales posting double-digit growth rates for seven consecutive months since November and the brisk pace of plantings for the just-commenced kharif (monsoon) crop season only reinforce the point.

Agriculture’s newfound importance also possibly accounts for the two recent reforms that may not have come about in normal times. The first one does away with the government’s powers to impose stockholding limits on cereals, pulses, potatoes, onions, edible oils, and other foodstuffs, save under “extraordinary conditions” of war, famine, or annual retail price increases above 50 percent. Such stock controls under ECA will, moreover, not apply to food processors and exporters. The second reform allows the sale and purchase of farm produce to take place outside the physical boundaries of regulated wholesale markets. That, in theory, would give farmers the freedom to sell directly to processors, traders, or retailers within and outside their states, including through electronic trading platforms.

These reforms—especially the one removing ECA stockholding limits, which ironically received a fresh lease on life under this very government—are significant from a signaling standpoint about a sector that is no longer supply-constrained. It required an economic crisis, which COVID-19 brutally lay bare, to recognize the value and potential of Indian farming and agri-business.

Harish Damodaran is National Rural Affairs and Agriculture Editor of The Indian Express and was a CASI Spring 2008 Visiting Scholar. He is especially grateful to Mekhala Krishnamurthy and Arvind Subramanian for their valuable inputs and comments.

India in Transition (IiT) is published by the Center for the Advanced Study of India (CASI) of the University of Pennsylvania. All viewpoints, positions, and conclusions expressed in IiT are solely those of the author(s) and not specifically those of CASI.

© 2020 Center for the Advanced Study of India and the Trustees of the University of Pennsylvania. All rights reserved.